Merchants spend hundreds of billions of dollars every year to process payments. The latest Nilsen Report on merchant payment processing fees in the US found processing fees topped $160 billion in 2022. In the UK, a British Retail Consortium survey over the same period found UK retailers alone paid over £1 billion in fees to accept card payments online.

While these payment fees are part of the cost of doing business, that doesn’t stop the CFO or Finance Director from asking if there’s a way to lower payment processing costs.

If that’s a question you’ve faced recently, or if reducing the cost of payment acceptance has become a key KPI, then this article is for you. We’ll be exploring the:

- Different types of payment fees

- Various fee structures you may encounter

- Strategies and tactics you can deploy to reduce your payment costs

Unpacking the cost of a card payment

The cost to process a typical payment is broken down into three categories. While these fees compromise the bulk of what merchants pay to process a payment, other costs may also exist.

- Interchange Fees are typically the largest line item of the invoice you’ll receive. They are charged by the bank issuing the customer’s card, which amounts to a percentage of the transaction value (sometimes, there may also be a fixed fee). The actual rate charged depends on various factors, including the card type, where the payment is made, and the business Merchant Category Code (MCC), but typically, they sit between 0.3% and 2% of the total transaction cost.

- Assessment fees are what you pay to the card networks for using their service. They are usually around 0.12-0.15% of the total transaction value.

- Processor fees are charged by the Payment Service Provider (PSP) you use. Each PSP will have distinct fee structures and will likely adjust these based on your business, average order value, and risk profile. Some processors charge a minimum monthly fee and may charge additional fees for additional services like fraud checks.

- Chargeback fees are a cost of accepting card payments. They occur when a customer successfully disputes a transaction. Depending on your agreement with your acquirer, the cost of chargebacks can range between $20 and $100.

As you can see, many variables are involved in the cost of processing a payment, and it’s critical to understand the amount you’re paying and what the payment is for. For this reason, many businesses have moved to an Interchange++ (IC++)pricing model. Unlike its alternative ‘blended pricing’ model, IC++ pricing gives merchants a complete breakdown of costs and the ability to reduce these by changing how they process their payments.

Blended pricing versus ICC++

How to reduce card payment fees

Merchants spend hundreds of billions of dollars every year processing payments. The latest Nilsen Report on merchant payment processing fees in the US found that processing fees topped $172 billion in 2023. In the UK, a British Retail Consortium survey over the same period found that UK retailers alone paid over £1.64 billion in fees to accept card payments online.

While debit and credit card processing fees are part of the cost of doing business, that doesn’t stop the CFO or Finance Director from asking if there’s a way to lower payment processing costs.

If that’s a question you’ve faced recently, or if reducing the cost of payment acceptance has become a key KPI, then this article is for you. We’ll be exploring the different types of payment fees, various fee structures you might encounter, and strategies you can use to reduce your payment costs.

Reducing card payment fees through traditional means can be resource-intensive. Primer, a unified payment infrastructure, makes it easy. Check out our demo to see how Primer works, or book a call with one of our payment experts.

Unpacking the cost of a card payment

The cost to process a typical payment is broken down into four categories. While these fees compromise the bulk of what merchants pay to process a payment, other costs may also exist.

- Interchange Fees are typically the largest line item of the invoice you’ll receive. They are charged by the bank issuing the customer’s card, which amounts to a percentage of the transaction value (sometimes, there may also be a flat fee). The actual rate charged depends on various factors, including the type of card, where the payment is made, and the business Merchant Category Code (MCC), but typically, they sit between 0.3% and 2% of the total transaction cost.

- Assessment fees are essentially a service fee. They are usually around 0.12-0.15% of the total transaction value.

- Processor fees are charged by the Payment Service Provider (PSP) you use. Each PSP will have distinct fee structures and will likely adjust these based on your business, average order value, and risk profile. Some processors charge a minimum monthly fee and may charge additional fees, such as for extra services like fraud checks.

- Chargeback fees are a necessary cost of processing debit and credit card transactions. They occur when a customer successfully disputes a transaction. Depending on your agreement with your acquirer, the cost of chargebacks can range between $20 and $100.

As you can see, many variables affect the cost of processing a payment, and it’s critical to understand the amount you’re paying and what the payment is for.

For this reason, many businesses have switched to an Interchange++ (IC++)pricing model. Unlike its alternative, ‘blended pricing,’ IC++ pricing gives merchants a complete breakdown of costs and the ability to reduce them by changing how they process their payments.

Blended pricing versus ICC++

Let's look at the pros and cons of the two pricing models in payments.

Blended advantages:

- Simplified processing: No need to track or analyze complex interchange fees.

- Predictable costs: Easier budgeting, as merchants can forecast processing fees.

- Potential savings: Beneficial for businesses with a consistent card mix or low transaction volumes.

Blended disadvantages:

- Limited flexibility: Merchants have less control over fee structures and can’t adapt to interchange rate changes.

- Higher costs for high-volume merchants: This may result in more expensive fees than IC++.

- Lack of transparency: Merchants cannot see the breakdown of interchange fees.

IC++ advantages:

- Full cost transparency: Merchants can see a detailed breakdown of interchange, scheme, and processor fees.

- Potential cost savings: This can be more cost-effective for businesses with high transaction volumes.

- Greater flexibility: Merchants can negotiate fees and optimize their payment costs.

IC++ disadvantages:

- More complex: Requires tracking and managing interchange fees individually.

- Slower settlements: Payments may take 2–3 days to fully settle as processors wait for fee data from card networks and issuers.

- Variable costs: Transaction fees fluctuate based on card type, transaction type, and interchange rates.

Seven ways to reduce the cost of payments

Let's look at some steps you can take to reduce your payment fees.

1. Develop a multi-acquirer strategy

This means working with multiple payment service providers instead of using just one. It gives you more flexibility and control, allowing you to choose the most cost-effective payment option while keeping your approval rates steady. Plus, having multiple providers competing for your business can help you negotiate better deals.

Learn more about the benefits of developing a multi-acquirer payment strategy.

2. Use the most cost-effective routing and domestic payment rails

Payment fees differ depending on the payment method used. You can reduce costs and improve financial efficiency by choosing the best payment route for your business and market—especially to avoid cross-border fees. You may also operate in markets where domestic card schemes exist. For example, payments made using Cartes Bancaires in France are significantly cheaper than those made with Visa or Mastercard. If these local schemes are available, it’s smart to encourage customers to use them since they’re more affordable.

Learn more about how Primer enables you to accept domestic card payments.

3. Provide cheaper payment options and encourage customers to use them

The payment industry is constantly changing, with more options becoming available and many cheaper than traditional credit and debit card payments. One key example is account-to-account (A2A) payments.

ACH in the US, SEPA Instant in Europe, Pix in Brazil, and iDEAL in the Netherlands have lower transaction costs because they eliminate intermediaries. Businesses can save significantly by offering A2A payment options and encouraging customers to use them, especially for high-value transactions.

4. Include sufficient data to qualify for lower interchange rates in unregulated markets

Issuers consider transactions that include extra data less risky and may qualify for lower interchange fees. In the US, for example, collecting a customer's ZIP code and passing this on to an issuer can reduce interchange fees by 1% or even more. Level II and Level III data is another option for businesses selling to other businesses.

5. Optimize fraud prevention and reduce chargebacks

Fraud poses a significant direct expense for merchants, amplifying payment fees as an indirect consequence. PSPs and issuers view merchants with high fraud rates unfavorably, often imposing premium charges for accepting payments. Thus, mitigating fraud and chargebacks emerges as a strategic avenue for curbing the expenses associated with payment acceptance.

6. Use the correct Merchant Category Code (MCC)

MCCs are four-digit numbers that classify the type of goods or services a business provides. These codes directly impact a merchant’s processing fees, as they help determine the applicable interchange rates and other charges. Businesses in lower-risk categories—those with fewer fraud cases and chargebacks—may qualify for lower fees. Merchants should use the correct MCC to ensure accurate transaction accounting and secure the best possible rates, especially if they operate in a low-risk industry.

7. Use Network Tokens

Using network tokens has been shown to reduce fraud and boost authorization rates, especially for card-not-present transactions, which are typically more susceptible to fraud. Even better, Visa and Mastercard have offered better pricing for payments made with these tokens since 2023. So, not only do you get enhanced security for online payments, but you also save money on processing fees as a merchant.

How Primer can help you reduce payment fees

Primer is a unified payment infrastructure that helps businesses manage, optimize, and scale online payments globally. Through a unified API, Primer consolidates multiple payment methods, processors, and tools into a single platform, empowering you to take complete control of your payment stack and transform complex payment processes into opportunities for growth.

Here are three ways Primer can help you save on processor fees:

1. Integrate with multiple payment processors and add new payment methods without any code

As we’ve mentioned, building a multi-acquirer payment strategy is crucial, especially if you want to optimize for cost. Of course, before you can route payments to the most cost-efficient provider, you need a simple way to add new processors.

However, adding new or switching payment processors typically involves complex integrations, requiring extensive engineering resources.

But once you’ve integrated with Primer, you can add new payment processors—both global and local providers—in just a few steps:

- In the Primer Dashboard, select the processor you’d like to use.

- Connect your existing processor account by granting Primer the necessary permissions.

- Choose any additional payment methods you want to associate with this processor.

- Adjust your universal checkout settings to decide how and when these methods appear for customers.

Adding additional payment methods is just as simple. You can pick from Primer’s extensive list of payment methods and integrate with them in just a few clicks.

You can then manage exactly which ones to offer customers through Universal Checkout.

With just a few clicks, you can turn on or off local and alternative payment options—ensuring you’re always providing the best payment experience at the lowest possible cost.

2. Optimize payment routing to reduce costs and improve success rates

Now that your processors and payment methods are ready, it’s time to streamline how payments are routed. Traditionally, routing logic—even for basic setups like region-specific processing—has been a complex, resource-heavy task requiring engineering input and constant maintenance.

Primer simplifies this with no-code Workflow Automation. We allow you to configure routing logic tailored to your needs, whether based on transaction value, customer location, or acquirer performance. For instance, you could route all French transactions to PayPug, a local French acquirer, while using Worldpay for payments outside that market.

Primer also makes setting up backup processors seamless with Fallbacks. If a transaction fails due to an issue with one acquirer, it’s automatically rerouted to another, ensuring payment continuity. This feature can recover a significant percentage of otherwise lost transactions, boosting both revenue and customer satisfaction.

Read more about Fallbacks here.

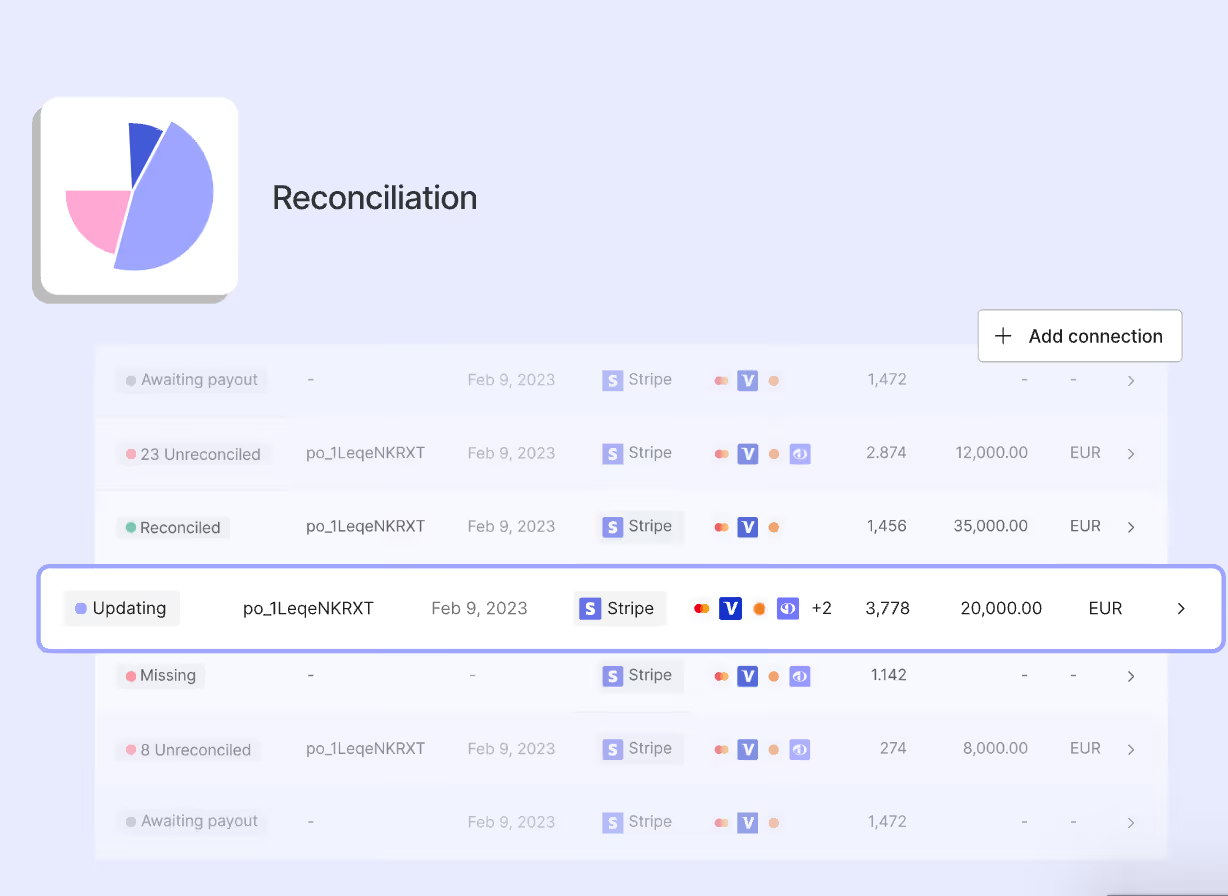

3. Identify and reduce unnecessary costs with Reconciliation

Reducing payment fees starts with having a clear, consolidated view of your payment costs—but fragmented systems can make it difficult to track transaction costs and spot inefficiencies. Without visibility into settlement reports, processor fees, and acquirer behavior, opportunities to save often go unnoticed.

Primer’s Reconciliation tool brings all your payment data into a unified view, helping you accurately track and analyze fees across processors. With real-time insights into transaction settlements and financial performance, you can identify where costs are adding up and take action to optimize your payment strategy.

How AppsFlyer use Primer to reduce payment costs

AppsFlyer, a prominent name in marketing measurement and analytics, sought to enhance its payment operations to boost efficiency and cut expenses. Traditionally, B2B transactions have relied on standard payment methods, often resulting in elevated processing fees and limited client flexibility.

By collaborating with Primer, AppsFlyer revamped its payment approach. They incorporated economical payment options like digital wallets and Open Banking, which generally incur lower transaction fees than traditional debit or credit card payments. This strategy expanded payment choices for clients and notably decreased processing expenses.

Primer's no-code workflow automation also empowered AppsFlyer to establish intelligent payment routing. This system directed transactions through the most cost-effective channels, further reducing fees. The capability to manage and refine payment flows without significant engineering involvement enabled AppsFlyer to implement these adjustments promptly and effectively.

Through this partnership, AppsFlyer streamlined its payment processes and achieved substantial savings in payment processing fees, illustrating the advantages of utilizing Primer's infrastructure.

Read the full case study here: How AppsFlyer Redefined B2B Payments with Primer.

With Primer, payments aren't a cost center

While working to reduce the cost of accepting payments is worthwhile, it’s important to remember that payments aren’t a cost center—they’re a strategic asset. It’s often the case that the revenue gains merchants get from optimizing their payment processing outweigh the cost savings they’d make.

Look at our ROI Calculator to see for yourself, and book a call with our experts to find out how Primer can help your business optimize your payments strategy. take a look at the pros and cons of the two pricing models that exist in payments.

Blended advantages:

- Simplified payment processing because there is no need to track and analyse complex interchange fees

- Predictable costs and budgeting because merchants can forecast processing fees

- Potential savings for merchants with a consistent card mix or low transaction volumes

Blended disadvantages:

- Less flexibility to negotiate fee structures or respond to changes in interchange fees

- Potentially higher fees for merchants with large transaction volumes

- Poor transparency as merchants cannot see the interchange fees

IC++ advantages:

- Transparency as merchants can see a complete breakdown of costs

- Potential savings for merchants with high transaction volumes

- More flexibility for merchants to negotiate individual fees

IC++ disadvantages:

- More complexity as merchants may need to track and manage interchange fees individually

- Settlements can be slow as it may take two to three days for a payment processor to receive the fee data from card networks and issuing banks

- Transaction rates can vary

Seven ways to reduce the cost of payments

Let's take a look at some steps you can take to reduce your payment fees.

Develop a multi-acquirer strategy

This entails collaborating with multiple payment service providers to avoid reliance on a single pricing model. This approach affords you enhanced flexibility and autonomy, enabling you to select the most cost-effective payment route while ensuring consistent authorization rates. Additionally, operating within a competitive landscape empowers you to negotiate more advantageous terms with providers.

Learn more about the benefits of developing a multi-acquirer payment strategy.

Use the most cost-effective routing and domestic payment rails

Fees vary between different payment rails, and by selecting the most suitable payment route for your business and markets, mainly to avoid cross-border charges, you can minimize costs and improve overall financial efficiency. You may also operate in markets where domestic card schemes exist. For example, payments made using Cartes Bancaires are significantly cheaper than those made with Visa or Mastercard. So, if it’s an option, you’ll want to encourage customers to use these schemes as they’re more cost-effective.

Learn more about how Primer enable you to accept domestic card payments.

Provide cheaper payment options and encourage customers to use them

The payment landscape constantly evolves, with an expanding array of options available. Account-to-account (A2A) payments represent a prime example of this evolution. ACH in the US, SEPA Instant in Europe, Pix in Brazil, and iDEAL in The Netherlands have lower transaction costs due to fewer intermediaries involved. Incorporating A2A payment options and encouraging customer adoption can deliver substantial cost savings, especially on large-ticket transactions.

Include sufficient data to qualify for lower interchange rates in unregulated markets

Transactions sent to issuers that include additional data are seen by issuers as less risky and can qualify for lower interchange fees. In the US, for example, collecting a customer's ZIP code and passing this on to an issuer can reduce interchange fees by 1% or even more. Level II and Level III data is another option for businesses selling to other businesses.

Optimize fraud prevention and reduce chargebacks

Fraud poses a significant direct expense for merchants, amplifying payment fees as an indirect consequence. Payment service providers (PSPs) and issuers view merchants with high fraud rates unfavorably, often imposing premium charges for accepting payments. Thus, mitigating fraud and chargebacks emerges as a strategic avenue for curbing the expenses associated with payment acceptance.

Use the correct Merchant Category Code (MCC)

MCCs are four-digit numbers that classify the type of goods or services a business offers. This data helps to determine the relevant interchange fee and other related charges. A business in a less risky category with lower fraud rates and fewer chargebacks might qualify for a lower rate. Merchants must ensure they have the correct codes for accurate transaction accounting and to gain the most favorable rates if they have low-risk businesses.

Use Network Tokens

Using network tokens has been shown to reduce fraud and boost authorization rates. Even better is that Visa and Mastercard offer better pricing for payments made with these tokens since last year. So, not only do you get better security, but you also save money on processing fees as a merchant.

Payments aren't a cost centre

While working to reduce the cost of accepting payments is worthwhile, it’s important to remember that payments aren’t a cost center; they’re a strategic asset. It’s often the case that the revenue gains merchants get from optimizing their payment processing outweigh the cost savings they’d make.

Take a look at our ROI Calculator to see for yourself.

.avif)